Is a professionally managed investment fund that pools money from many investors to purchase securities. These investors may be retail or institutional in nature. Mutual funds have advantages and disadvantages compared to direct investing in individual securities.

are close-ended, lock-in period of 3 years diversified equity schemes offered by mutual funds in India. They offer tax benefits under the new Section 80C of Income Tax Act 1961. ELSS can be invested using both SIP and lump sums investment options.

are close-ended, lock-in period of 3 years diversified equity schemes offered by mutual funds in India. They offer tax benefits under the new Section 80C of Income Tax Act 1961. ELSS can be invested using both SIP and lump sums investment options.

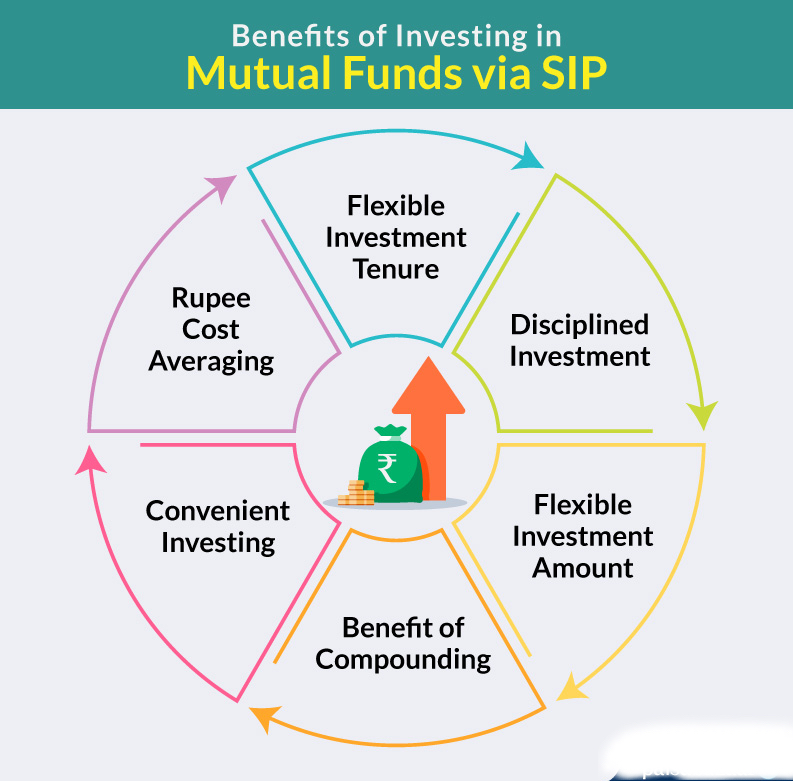

SIP is an investment option offered by many mutual funds to investors, allowing them to invest small amounts periodically instead of lump sums. The frequency of investment is usually weekly, monthly or quarterly.

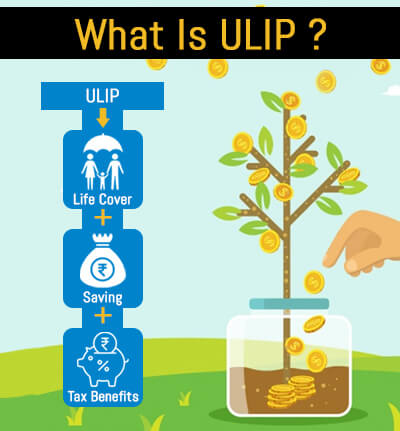

ULIP is a combination of investment & life insurance. Here policyholder can pay a premium monthly or annually. A small amount of the premium goes to secure life insurance and rest of the money is invested just like a mutual fund does. ULIPs are best suited for individuals with a long term financial plan of wealth creation and insurance. Whether it is for retirement, children’s education or for other financial goals, a ULIP continued till maturity works as an advantage. It gives you the dual benefit of savings and protection, all in a single plan. ULIP returns and/or maturity is also exempted from tax so they are also a good tool to save tax. However, contact your financial advisor for up to date information.

ULIP is a combination of investment & life insurance. Here policyholder can pay a premium monthly or annually. A small amount of the premium goes to secure life insurance and rest of the money is invested just like a mutual fund does. ULIPs are best suited for individuals with a long term financial plan of wealth creation and insurance. Whether it is for retirement, children’s education or for other financial goals, a ULIP continued till maturity works as an advantage. It gives you the dual benefit of savings and protection, all in a single plan. ULIP returns and/or maturity is also exempted from tax so they are also a good tool to save tax. However, contact your financial advisor for up to date information.

An endowment plan combination product of investment and life insurance. It is an investment product that you buy from a life assurance company. The policy includes life assurance, so it will also pay out if the individual expires during the term & if you outlive the entire policy tenure, the insurer will pay out the sum assured as the maturity benefit too. It’s a contract designed to pay a lump sum after a specific term or on death. Typical maturities are ten, fifteen or twenty years up to a certain age limit. Some policies also pay out in the case of CI (critical illness). Policies are typically traditional with-profits or unit-linked. They have flexibility to match your budget offering different PPT (premium payment term). Endowment policy also plays a role in tax planning as earned amount in the form of interest, bonus and/or maturity may be exempted from tax. Contact your financial advisor for up to date information

An equity investment is money that is invested in a company by purchasing shares of that company in the stock market. These shares are typically traded on a stock exchange. Equity essentially means ownership. By doing so, investors are forming a partnership with the companies they choose to invest in – if the company makes profit, investors earn returns proportionate to the amount of equity they purchased; if the company suffers a loss, the investors lose the money proportionally. They have the potential to give you the highest returns but comes with its own set of risks. Equity Investments can save tax also but the Government rules pertaining to tax are volatile. Contact your financial advisor to get an update on the same.

An equity investment is money that is invested in a company by purchasing shares of that company in the stock market. These shares are typically traded on a stock exchange. Equity essentially means ownership. By doing so, investors are forming a partnership with the companies they choose to invest in – if the company makes profit, investors earn returns proportionate to the amount of equity they purchased; if the company suffers a loss, the investors lose the money proportionally. They have the potential to give you the highest returns but comes with its own set of risks. Equity Investments can save tax also but the Government rules pertaining to tax are volatile. Contact your financial advisor to get an update on the same.

A bond is a debt security, in which the authorised issuer – company, financial institution, or Government, offers regular or fixed payment of interest in return for the money borrowed by the said issuer. It is for a certain period of time.

Is a financial instrument provided by banks or NBFCs which provides investors a higher rate of interest than a regular savings account, until the given maturity date. It may or may not require the creation of a separate account.

Is a financial instrument provided by banks or NBFCs which provides investors a higher rate of interest than a regular savings account, until the given maturity date. It may or may not require the creation of a separate account.